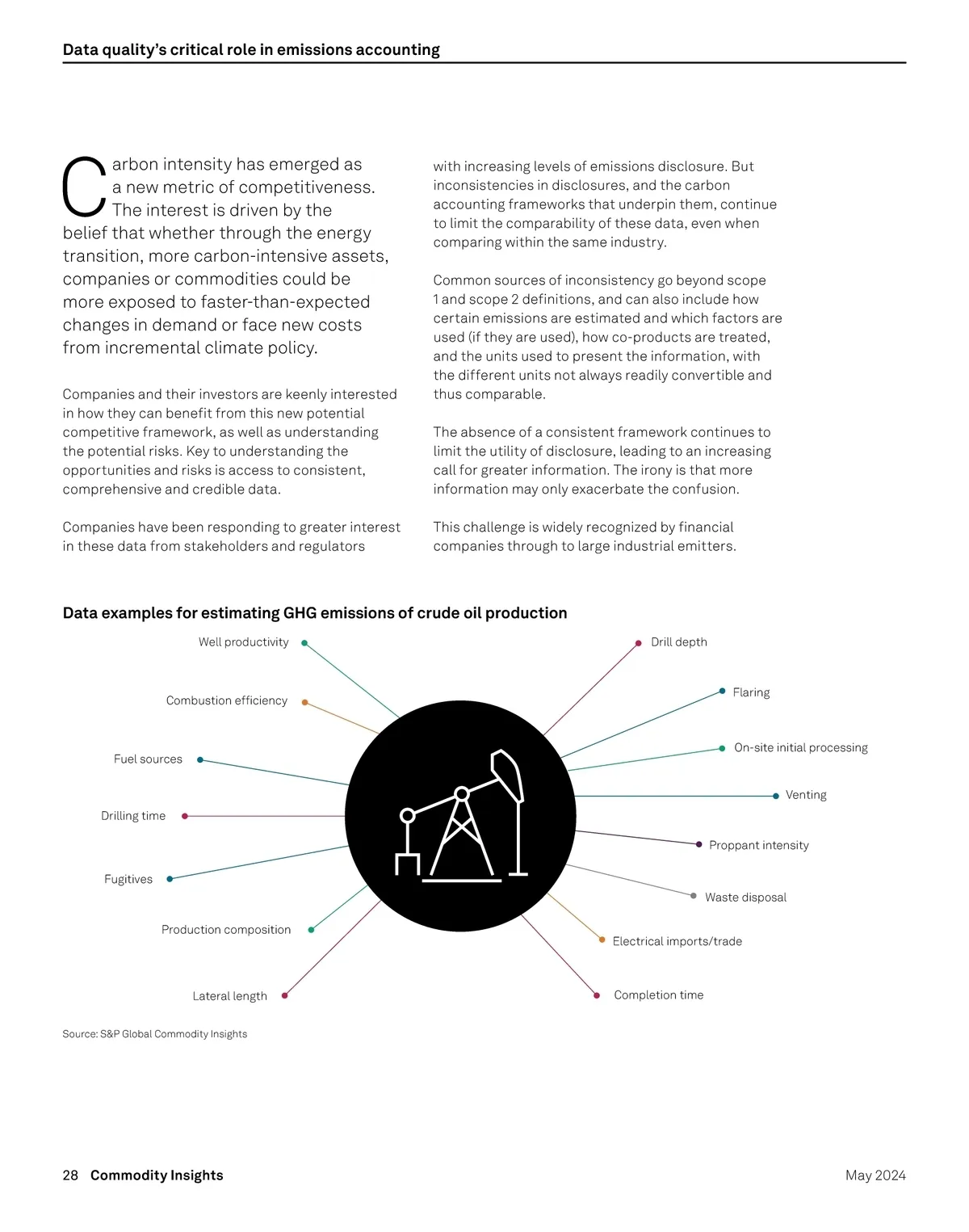

Data quality’s critical role in emissions accounting C arbon intensity has emerged as a new metric of competitiveness. The interest is driven by the belief that whether through the energy transition, more carbon-intensive assets, companies or commodities could be more exposed to faster-than-expected changes in demand or face new costs from incremental climate policy. with increasing levels of emissions disclosure. But inconsistencies in disclosures, and the carbon accounting frameworks that underpin them, continue to limit the comparability of these data, even when comparing within the same industry. Common sources of inconsistency go beyond scope 1 and scope 2 definitions, and can also include how certain emissions are estimated and which factors are used (if they are used), how co-products are treated, and the units used to present the information, with the different units not always readily convertible and thus comparable. The absence of a consistent framework continues to limit the utility of disclosure, leading to an increasing call for greater information. The irony is that more information may only exacerbate the confusion. This challenge is widely recognized by financial companies through to large industrial emitters. Companies and their investors are keenly interested in how they can benefit from this new potential competitive framework, as well as understanding the potential risks. Key to understanding the opportunities and risks is access to consistent, comprehensive and credible data. Companies have been responding to greater interest in these data from stakeholders and regulators Data examples for estimating GHG emissions of crude oil production Well productivity Drill depth Combustion efficiency Flaring Fuel sources On-site initial processing Venting Drilling time Proppant intensity Fugitives Waste disposal Production composition Electrical imports/trade Lateral length Source: S&P Global Commodity Insights Completion time 28 Commodity Insights May 2024

Commodity Insights Conventional and new energy in focus: Page 28