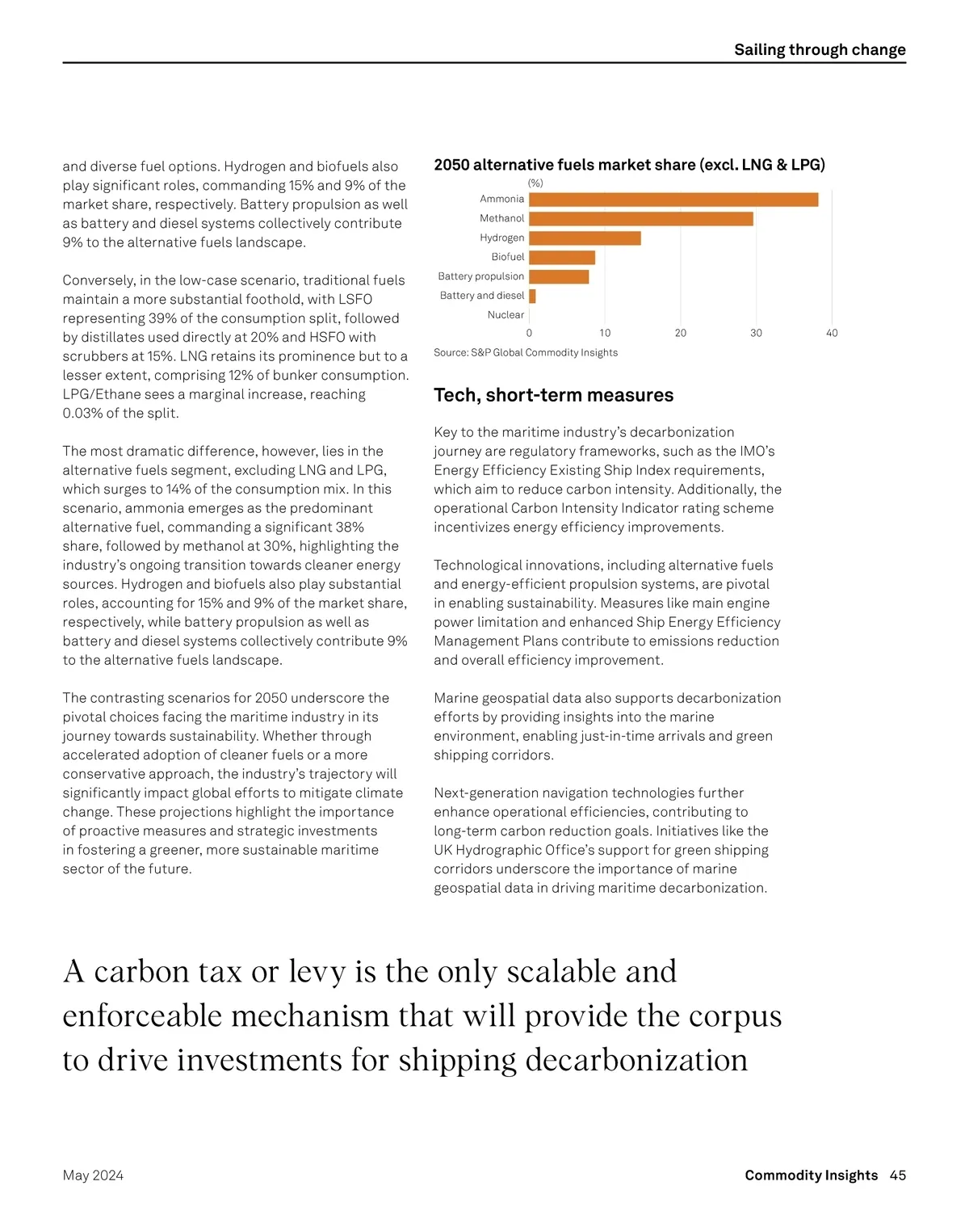

Sailing through change T he shipping industry is the bedrock of global commerce. It plays a vital role in keeping the wheels of world economy turning, with over 90% of traded goods carried by ships. 2050: a multifuel future Future fuel availability is also a focus in S&P Global Commodity Insights’ latest Maritime Forecast to 2050 report, which outlines the conditions under which each new fuel type will proliferate. What will win – ammonia vs methanol, biofuels, e-fuels or fossil fuels with carbon capture and storage – remains uncertain, but we can say with confidence that the future fuel market will be more diverse than today and reliant on multiple primary energy sources. In the envisioned maritime landscape of 2050, two contrasting scenarios present divergent trajectories for bunker consumption and alternative fuels utilization. In the high-case scenario, the consumption split portrays a marked shift away from traditional fuels, with low sulfur fuel oil (LSFO) accounting for a reduced 13%, while distillates used directly and high sulfur fuel oil (HSFO) with scrubbers witness declines to 12% and 3%, respectively. Meanwhile, LNG emerges as a dominant player, capturing a 32% share, indicative of a substantial embrace of cleaner energy sources. LPG/Ethane, previously negligible, makes a notable appearance, constituting 1% of the consumption split. However, a most striking transformation unfolds within the alternative fuels’ domain, excluding LNG and LPG, which skyrockets to 39% of the consumption mix. Among these alternatives, ammonia claims the largest share at 38%, followed by methanol at 30%, demonstrating a decisive shift toward sustainable Ships are widely regarded as one of the most cost-and carbon-efficient means of transport, yet more needs to be done to reduce shipping’s carbon footprint as it accounts for about 3% of global greenhouse gas (GHG) emissions. With global trade expected to grow ahead of the global economy, the associated emissions are also expected to rise. An intense spotlight has been thrown on shipping’s global role in emissions in the past few years and the industry faces a multitude of challenges in the years ahead as it moves toward net zero. The International Maritime Organization (IMO), shipping’s governing body, has set ambitious targets to reduce GHG emissions from ships and there is a strong political will to phase them out as soon as possible. The most ambitious of these targets is having member states adopt the 2023 IMO Strategy on Reduction of GHG Emissions from Ships, with enhanced targets to tackle harmful emissions. As pressure mounts to deliver measurable progress toward carbon neutrality, IMO is pledging to reach net zero by or around 2050. Many types of alternative fuels are being explored for shipping, such as ammonia, methanol, Biofuels, hydrogen and fuel cells, but there is no one clear frontrunner in the race. Meanwhile, cargo owners are looking to decarbonize their supply chains while shipping companies are embarking on a major transition from conventional to climate-friendly carbon-neutral fuels, having placed early bets on green methanol and bio-LNG, among others. The industry, however, will need to understand the key drivers and implications of a new multifuel future. 2050 bunker consumption split 100 80 60 40 20 0 (%) Alternative fuels (ex LNG & LPG) LNG HSFO (Scrubber) Distillates used directly LSFO LPG/Ethane Reference case Higher alternative fuel uptake case Source: S&P Global Commodity Insights 44 Commodity Insights May 2024

Commodity Insights Conventional and new energy in focus: Page 44